Check Fraud is Up: 4 Steps to Protect Yourself

Check Fraud Is Rising: Here’s How to Stay Safe

What to Know:

- The Risk: Check fraud claims nearly doubled despite fewer checks being written. Criminals steal mail and “wash” checks to cash them.

- Protect Yourself: Reduce check use, write with indelible ink, monitor accounts online, and mail checks at the post office.

- Best Move: Digital payments (Bill Pay, Zelle®, ACH) can be safer than paper checks.

Check Fraud is Up

Check fraud is on the rise. In 2024, there were more than 680,000 claims of potential check fraud, nearly double the previous year, according to the American Association of Bankers. (By comparison, in 2014, there weren’t even 97,000 such claims.)1 And this is in the face of declining paper check writing by American consumers – according to the Federal Reserve, check use by individuals has been in decline since 2000.2

How does the current fraud work?

It’s fairly low tech. Fraudsters will steal mail out of people’s mailbox, or steal a key from the postal service that gives them access to the blue mailboxes on the corner. They’ll go through the mail, pull out checks and engage in “check washing,” a process by which the payee and amount of the check is wiped off the check itself. Typically, this is done with nail polish remover, or another common household chemical.

The fraudster then either sells the blank checks online, or writes in an amount and recruits someone to deposit them, or deposits the checks themselves. Once a check has funds available associated with it, the funds are immediately withdrawn as cash, often at an ATM.

Four things you can do to protect yourself

First off, if you identify check fraud in your account, contact your bank immediately. Also, file a report with the Postal Inspection Service and your local police. In many cases, you’ll eventually be made whole, provided you caught the fraud soon enough. Situations do vary, though. Talk with your bank should it happen to you.

Sound like something you’d rather avoid? Here’s how.

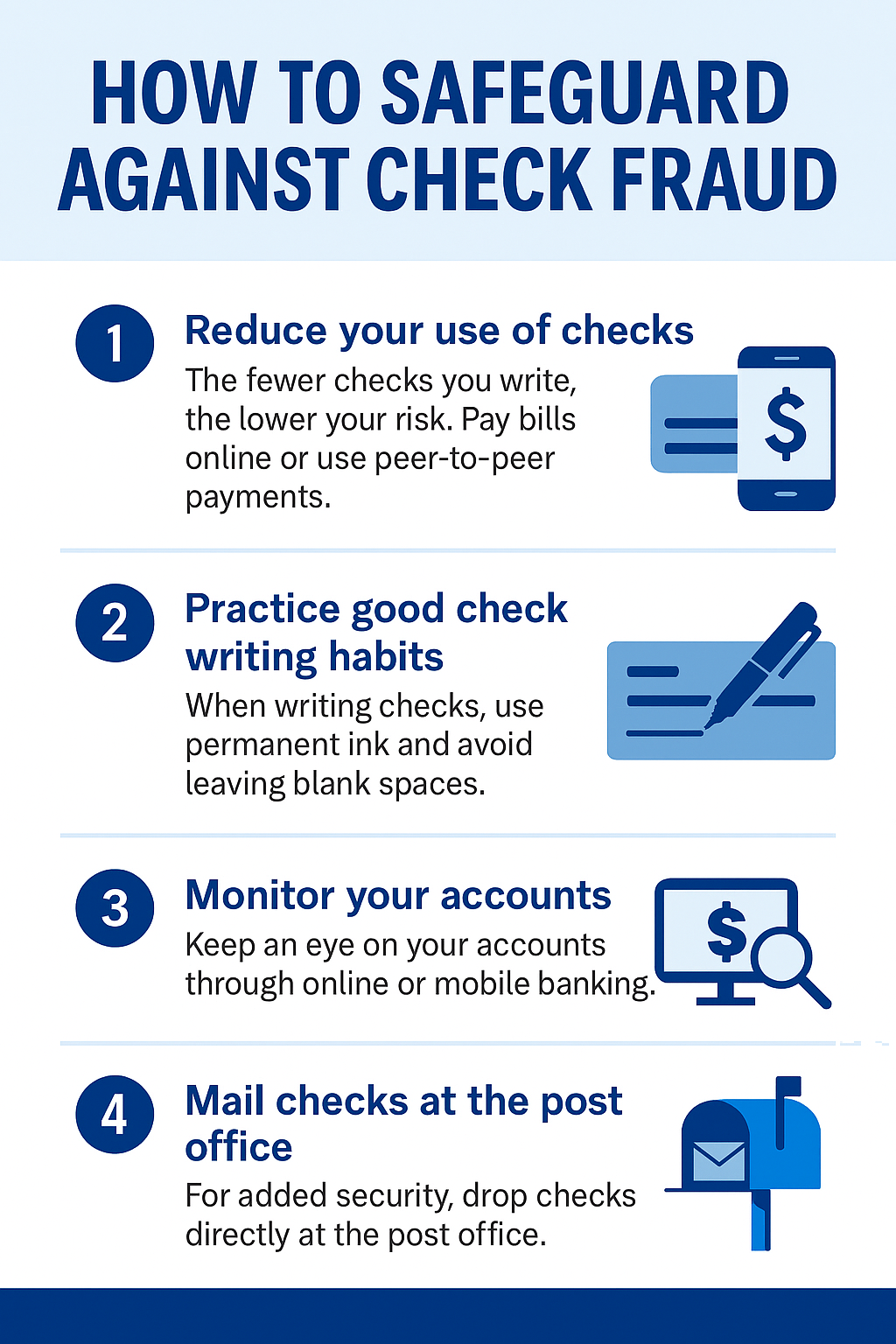

1. Reduce your use of checks. The fewer checks you write, the lower your risk. If you’re still paying bills with paper checks, most companies have online payment solutions available to their clients. In fact, almost all companies do it online instead. Or, your bank likely offers a Bill Pay tool, if you’d rather set up all your payments on one dashboard. And, once you set it up, either alternative method is faster for you: no more handwriting checks, finding stamps and putting envelopes in the mail.

1. Reduce your use of checks. The fewer checks you write, the lower your risk. If you’re still paying bills with paper checks, most companies have online payment solutions available to their clients. In fact, almost all companies do it online instead. Or, your bank likely offers a Bill Pay tool, if you’d rather set up all your payments on one dashboard. And, once you set it up, either alternative method is faster for you: no more handwriting checks, finding stamps and putting envelopes in the mail.

Even service providers like lawn care providers, newspaper delivery people, plumbers and roofers often prefer a peer-to-peer payment system like Zelle®. It saves them a trip to the bank, and the hassle of keeping track of paper checks. You can often track the security of the payment by paying them on-the-spot, so they can confirm their details and receipt of payment.

Also realize that a check has a lot of personal information on it: your full name, address, bank account number, and what your signature looks like. While it’s not covered here, a check would be a good starting point for someone interested in committing identity theft. Better to have fewer of them circulating.

2. Practice good check writing habits. If you must write a check, use indelible ink, so it’s harder to wash. Don’t let there be any blank spaces in front of the payment amount. And never write a blank check, no matter how much you trust the person you’re giving it to.

3. Monitor your accounts. If you spot something fishy, report it immediately. The best way to track your accounts is through online or mobile banking. You’ll see things sooner. This is much safer and more effective than waiting for paper statements – paper statements are only sent once a month! (We also recommend the safety and ease of estatements.)

If you have checks out with others, track them digitally and make sure they get deposited. If a check hasn’t been deposited for a while, ask about it. If it wasn’t received, you can stop the check.

4. Mail checks at the post office. Ideally, you’d drop your sensitive mail off at the post office. If that’s not practical, put it in a blue mailbox before the last day’s pickup, so it’s not vulnerable overnight. Also, avoid putting up the flag on your mailbox and leaving checks in there for the mail carrier to pick up – that’s an easy one for thieves.

Why is check fraud on the rise?

Experts attribute it to several factors. During the pandemic, criminal scamming rings were formed to take advantage of stimulus payments. Once that source of fraud dried up, basic check fraud became a target.3 The dark web, or messaging apps like Telegram, enable coordination amongst fraudsters, so that washed checks or stolen mailbox keys can be sold quickly and easily, making the transition to check fraud relatively simple.1

Two other factors are also at play. First, the banking industry has spent a lot of time and money securing online and digital payments. Those forms of payment are actually quite safe, provided they’re made to the correct party. Check writing, however, is low tech and has been declining over the past several decades.

Second, the U.S. Postal Inspection Service has limited funding, according to a report by NPR.4 This is the organization responsible for the security of the mail. With fewer resources, it’s less able to secure the ubiquitous blue mailboxes. Less secure mail means more opportunity for fraudsters.

Key Takeaway: Alternative Methods Are Best

While you may need to occasionally write a check, it’s important to understand the risks – and how to protect yourself. When you have the option between paying by check, credit card, debit card, or an ACH transfer, realize that checks are by far the most vulnerable. The safest check is the one that’s not written at all.

Looking for more information on how to protect yourself from different types of fraud? Visit our fraud prevention page. We have tips on how to stay safe. At Old National, we’re committed to helping you guard against fraud.

1. “Back with a vengeance: the challenges of check fraud,” ABA Bank Journal. Published March 9, 2023. Accessed online May 5, 2023 at https://bankingjournal.aba.com/2023/03/back-with-a-vengeance-the-challenges-of-check-fraud/

2. “U.S. Consumers’ Use of Personal Checks: Evidence from a Diary Survey,” a research report published by the Atlanta Fed in 2020. Accessed online May 5, 2023 at https://www.atlantafed.org/-/media/documents/banking/consumer-payments/research-data-reports/2020/02/13/us-consumers-use-of-personal-checks-evidence-from-a-diary-survey/rdr2001.pdf

3. “Check fraud is on the rise. Here’s what you can do to prevent it.” New York Times. March 10, 2023. Accessed online May 5, 2023 at https://www.nytimes.com/2023/03/10/your-money/check-fraud-protection.html

4. “Check fraud is on the rise. Here's what you need to know and how to avoid it,” NPR Online, February 3, 2022. Accessed online May 5, 2023 at https://www.npr.org/2022/02/03/1077766541/usps-checks-mail-fraud-bank