217 results found

-

What should I do if I'm the victim of check fraud?

Check fraud occurs when someone steals your actual checks or reproduces them. They then attempt to cash those checks and, if successful, can pull money out of your account.

If you're the victim of check fraud, please visit any Old National banking center, as an associate will need to complete the appropriate paperwork, which will require your signature. At the same time, we will handle any changes that need to be made to your account. Sometimes it may be necessary to close the account and open a new one or issue a new debit card if the card number was compromised. -

What paperwork do you need from me to endorse an insurance claims check?

If you have damage to property that is financed through Old National, we will be an active part of your insurance claim process.The paperwork required and necessary steps differ based on the type of property. We have developed the guides you can download below to assist you:

Home mortgages

- Download our Guide to Homeowners Insurance Claims for an overview of the claim process, including documents you will need to provide and forms you should complete.

- Please note: This guide outlines processing insurance claims checks for HOME mortgages only (e.g. conventional first mortgages).

Consumer loans

For consumer loans, such as a vehicle or boat, quick home refi, home equity loans, including second mortgages, please use our Guide to Insurance Claims for Consumer Loans.Commercial loans

For commercial or business property, contact your Old National Bank commercial lender for guidance. -

What if I get an error message when I try to enroll an email address or U.S. mobile number in Zelle®?

Your email address or U.S. mobile phone number may already be enrolled with Zelle® at another bank or credit union. Call the Old National Client Care team at 1-800-731-2265 and ask them to move your email address or U.S. mobile phone number to Old National so you can use it for Zelle®.

Once Client Care moves your email address or U.S. mobile phone number, it will be connected to your Old National bank account so you can start sending and receiving money with Zelle® through Online or Mobile Banking.

Please call Old National Client Care toll-free at 1-800-731-2265 for help. -

What types of payments can I make with Zelle®?

Zelle® is a great way to send money to family, friends and people you are familiar with such as your personal trainer, babysitter or neighbor.1

Since money is sent directly from your bank account to another person's bank account within minutes,2 Zelle® should only be used to send money to friends, family and others you trust.

Neither Old National nor Zelle® offers a protection program for any authorized payments made with Zelle® — for example, if you do not receive the item you paid for or the item is not as described or as you expected.

1 Must have a bank account in the U.S. to use Zelle®.

2 Transactions typically occur in minutes when the recipient’s email address or U.S. mobile number is already enrolled with Zelle®. -

Someone sent me money with Zelle, how do I receive it?

If you have already enrolled with Zelle®, you do not need to take any further action. The money will be sent directly into your bank account and will be available typically within minutes.1

If you have not yet enrolled with Zelle®, follow these steps:

- Click on the link provided in the payment notification you received via email or text message.

- Select Old National.

- Follow the instructions provided on the page to enroll and receive your payment. Pay attention to the email address or U.S. mobile number where you received the payment notification — you should enroll with Zelle® using that email address or U.S. mobile number where you received the notification to ensure you receive your money.

1 Transactions typically occur in minutes when the recipient’s email address or U.S. mobile number is already enrolled with Zelle®.

-

How can I get a replacement for a broken or damaged debit card?

To order a replacement for a damaged debit card, call Client Care at 1-800-731-2265 or visit any banking center.

The normal timeframe for delivery is 7-10 business days. To receive a card sooner, you can instead choose to pay a $35 fee and receive the replacement card in two business days. The card must be ordered by 4pm on any business day for it to be delivered in two business days.

A Lost or Stolen Debit Card

If instead of a damaged debit card you need help with a lost or stolen card, please call us at 1-800-731-2265, option 2, in the US. You can report a lost or stolen card 24-hours a day. If you are outside of the US, call 1-812-422-2197. We can cancel or restrict your card, check for unauthorized transactions and order a new card for you. -

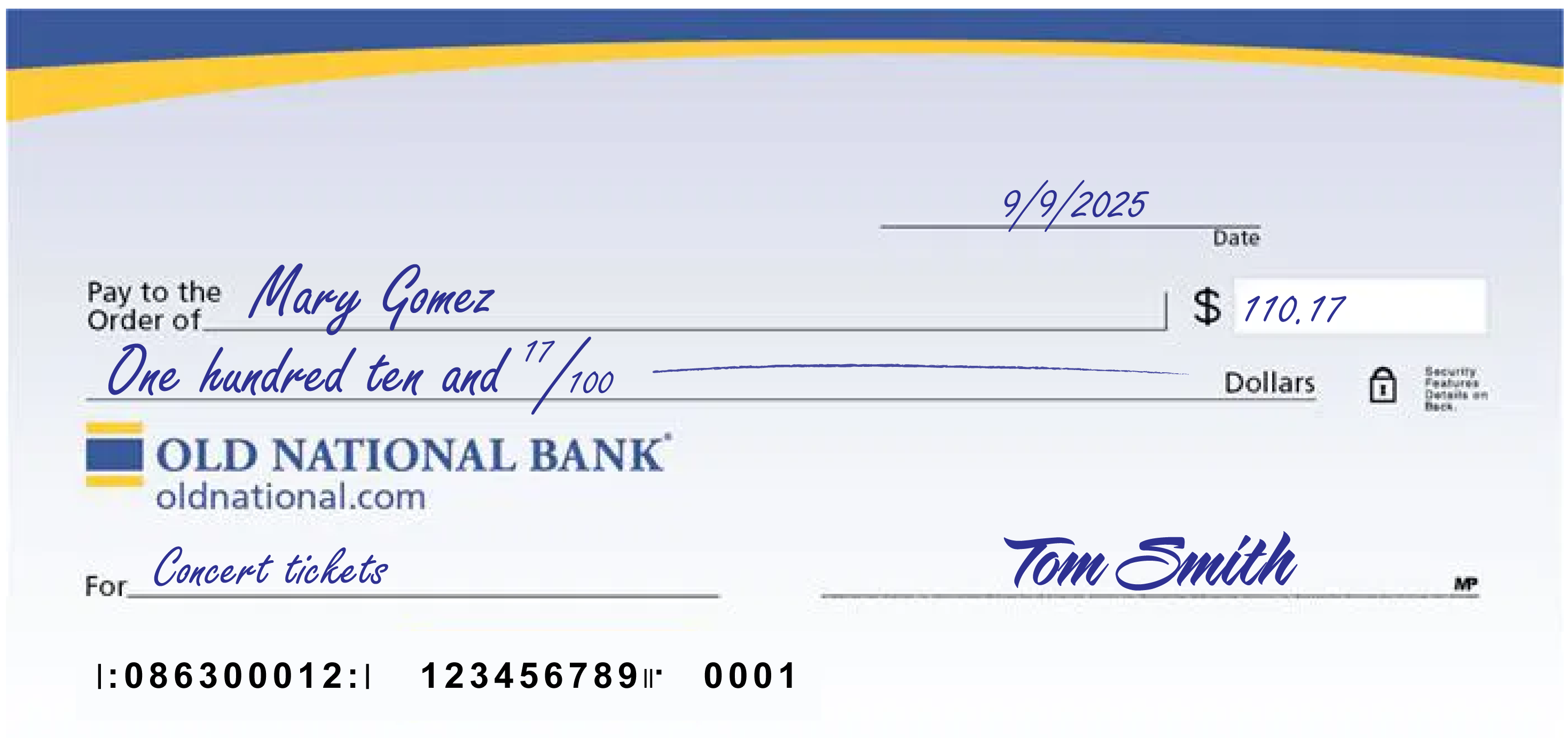

How do you write a check?

To write your check, fill out the fields carefully and sign at bottom right. We’ve included a properly filled out check below, as an example.

A few notes:

- The date at the upper right can be any standard format that includes the day, month and year.

- Write the full name of the person, business entity, or organization who is receiving the check in the “Pay to the Order of” field.

- The box at the right is for a numerical representation of the amount you’d like to pay the recipient.

- The line with “dollars” at the end is where you write out the amount you’d like to pay the recipient in words; write the cents as a fraction XX/100; if there’s extra space, draw a line until “dollars” so that no one can adjust the amount you wrote.

- The lower left field is for personal notes; this is optional. Some people like to write what the check is for, so they can remember when reviewing their records; If you’re paying a specific bill, you may be asked to write your invoice number or other identifying information you have on record with the company you’re paying.

- Sign the check at lower right with the signature that you use for all important documents.

- If you make a mistake on your check, you can cross it out and put your initials next to it and then write what you meant to write.

-

Why am I receiving calls regarding my loan account being past due when I have a grace period?

The grace period on your loan doesn't provide additional time beyond the due date to make a payment. The grace period only provides additional time before a late charge is assessed. If we don't receive your payment by the due date, it is considered late, and you may receive correspondence by phone or mail regarding the status of your payment.

-

How do I sign up for Online Bill Pay within Digital Banking?

Bill Pay is a free service that enables you to pay your credit card bill, cell phone bill, mortgage payment, utilities, individuals or really any bill you want to pay. Payment is taken directly from your Old National account. It's easy to begin using Online Bill Pay:

From a web browser

- Log in to Digital Banking

- Choose Pay or Transfer, then choose Bill Pay in the top menu

- You may need to enter a few pieces of identification, otherwise, review and check the box agreeing to the Terms & Conditions

- Click Complete Sign Up

- Begin adding information for the business or person you want to pay

Within Digital Banking, you can make one-time payments and set up automated, repeat payments. You can also enroll to receive eBills (electronic bills) from payees with Bill Pay and view your eBills history.

Please note: Depending on the party you are paying, payments may be sent electronically or a physical check will be produced and mailed.Our Bill Pay has its own FAQ as well. You can find it on the Bill Pay screen in the lower right corner under I want to. . .

In the Mobile App

- Open the Mobile App

- Choose Pay & Transfer, then choose Bill Pay

- Select Payees at the top right of the screen

- In the Add a person or business field begin adding information for those you want to pay

If you need assistance with enrolling in Bill Pay, please contact Client Care at 1-800-731-2265.

-

Can I open a checking account online?

We do provide a way to open most checking accounts online. Go to our Compare Checking Accounts page, find the account that best suits your needs and select the Open Account button.

We offer a variety of checking accounts to meet different needs. If you would like to talk to someone about the type of checking that would be best for you, please visit a banking center or call us at 1-800-731-2265.